By Peter @Newton Bell, 8 December 2016

Doug Ramshaw, Director of Vendetta Mining (TSX-V:VTT), joined me for an extensive conversation on the zinc markets recently and it is my pleasure to provide you with a transcript of our conversation below.

>>

P: Now, you sent me some material in advance of the call and I would like to try to summarize my broad impression about zinc so that you can correct any of my misunderstandings. Would it be OK for me to give you a quick summary of my understanding here?

D: Sure, Peter.

P: OK, thanks. I gather that there was a significant build-up in inventories over the past few years in both concentrate and finished metal around the world, attributed to the China-slow down. We’ve passed a point now where those buildups have started coming off – an inflection point, if you will. These inflection points can be interesting times for markets as prices can start to move significantly. The zinc prices are now high relative to the industry’s cost curve, so a lot of the producers are making money. You’re not really seeing the supply destruction that can set the stage for a massive bull run, but the supply-demand picture is fundamentally bullish for the zinc.

D: Well, yes and no. You’re right in terms of inventories, at least with the visible stocks. Zinc, like other metals, has a ghost inventory that no-one is completely sure about in terms of China. Visible LME stocks are off two-thirds in a pretty short period of time and that actually is a supply issue. What we saw coming into 2013 was, I feel, a somewhat unprecedented horizon for the non-Chinese metal supply situation. It started with Glencore Xstrata assets Perseverance and Brunswick in Canada shutting down in 2013. Then, last year, Century and Lisheen shut down. That was basically four of the world’s top eleven zinc mines shutting down in a two year span.

D: Whenever I’m talking about a world perspective, it’s generally outside of China. The Chinese production is small scale, but there is a lot of it. We saw four of the world’s top eleven zinc mines, by production, shut down in a two year span. They didn’t shut down because of low metal prices – this is crucial – they shut down because their resources were depleted. Those mines aren’t coming back. They represented close to 10% of world mine production. That was a huge supply issue and one that has led to an accelerated reduction in non-Chinese inventories of zinc.

D: Since those major mine retirements, we’ve seen a large drop in metals prices at the beginning of the 2016. That represented a fantastic buying opportunity on some stocks that are heavily leveraged to zinc; for example, Teck and Trevali. That price decline took some additional zinc production offline. Nyrstar basically reviewed all of its assets and a lot of that production is not coming back on in the short term. Glencore has made some temporary cutbacks, as well. Right now, the market is looking at prices where they are and wondering when Glencore might turn some of that production back on. Not withstanding some production coming back online, these production decreases are equivalent to Freeport and BHP Billiton exiting the copper market. Not for a year, or two years, but for good. It was very significant.

D: And because zinc prices were so low for so long, there really hasn’t been a lot of investment in the zinc business. There were a few primary zinc operations, but the metals prices have not supported the development of many zinc assets. It’s not just a short-term supply issue with mines shutting down; there is not a large amount of new zinc supply on the horizon from a Western point of view.

P: To ask a simple question here, would you say there was a relationship between that buildup in inventories and those mine closures?

D: All these closures were well-flagged, they were going to happen. There were some similarities here to the 2005-2007 run, which is one of the two runs the zinc market has had in the last 20 years. When you have a metal that is really off people’s radar, the first two mine closures didn’t really do much to the zinc market. The news was anticipated and those mine closures happened right on schedule. But the compound effect of Century and Lisheen coming off last year really seemed to have an effect on the markets. 2016 was, basically, the first calendar year where production was offline at all four of those mines. That represented a decrease of over one million tonnes of zinc production. That drove a big decline in LME stocks. Yes, I absolutely think that those supply cutbacks gave the market new teeth this year.

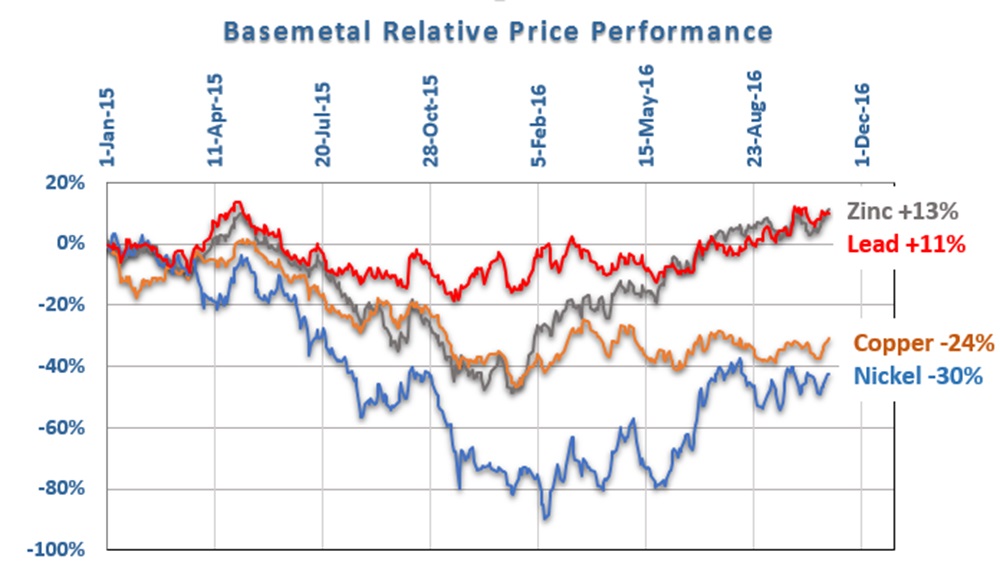

P: It looks like LME stocks were around 1.5M tonnes of zinc at their peak.

D: Yes, I think the peak was a little over 1.3M tonnes and we’re around 450,000 tonnes. We’re off two-thirds or more now.

P: OK. So, losing a million tonnes of annual production from those large mines is a big deal.

D: Yes and, this year, Nyrstar put their mining operations on hold. Glencore also had cutbacks. That was another 800,000 tonnes of decrease in zinc production this year. These were short-term cuts, but they added to the complete shutdowns. I have actually been caught a little off-guard with how the zinc price has accelerated this year. Zinc has traded up to $1.10 two or three times in the last five years, but it has peaked around there and then come back down. This year, it went through it like a hot knife through butter.

D: Zinc might have now run a little ahead of itself in the short term, but these are the kinds of moves that we, as a company, are anticipating next year and beyond. We’ve seen an almost doubling from the lows of earlier this year. Both the 2005-2007 run and the one in the late ‘80s saw, roughly, a quadrupling of zinc prices. We may be coming into the second half of this zinc move, but we believe there is still a way to go.

P: I can’t really wrap my head around losing annual production that is equivalent to the entire known stocks. What is global production?

D: Global production is around 13-14M tonnes right now. You add the temporary cuts this year to the complete shutdowns and you’re talking about 15% of that amount. Some of that will come back on, but you’ve hit the nail on the head.

D: Trying to time when the things turn can be a fools’ errand, but we are entering a period of deficits. We started up Vendetta a couple of years ago in anticipation of the zinc market. We may have been a little ahead of our time but, as an early adopter, you can get a headstart.

P: You mentioned that it is an unloved or unwatched market. It seems that zinc is mainly a contract-based market – it’s not so heavily traded on the US exchanges. Any comments on the plumbing of the zinc markets?

D: It’s funny – when I grew up in the UK, the big diversified mining corporation was RTZ Corporation. Of course, it’s now known as Rio Tinto PLC. All my time growing up, it was RTZ Corporation and the Z stood for zinc! It’s so unloved that a major company that had it in its name, for decades and decades, they have actually dropped it from its name. That’s why I think of it as the Rodney Dangerfield of metals – it just doesn’t get any respect.

D: It’s a big market. The copper market is north of 20M tonnes a year, which is larger, but it’s not like this is the boron market or something. Zinc production is significant. The only thing that gets me a little concerned is that over 50% of zinc is used in stainless steel in galvanizing steel. Although it’s not like steel is suddenly going to be obsolete.

D: As with any historical move in zinc, this will be no different. The bottom line is that there is an incentive price for production to come on stream. WoodMac have talked about that incentive price being around $1.30 in their modelling. People I respect greatly, who have much better knowledge of the Chinese production situation, have said that Chinese production can come on very quickly to take advantage of higher zinc prices. That’s what we’ve seen in the past. Anytime you have a strong market in something, it brings production on-stream that can actually curtail a longer-term bull run. But I think this move in zinc will be longer than the two-year cycles we’ve seen in the past. I think this zinc move does have legs.

D: You need to be in a position where you can take advantage of that zinc run. You want to have a project advanced to a point where it can be looked at as an M&A target. Breakwater was a great example of that – a lot of their producing assets were declining and Nyrstar couldn’t help themselves, in a bullish zinc frenzy, from making the acquisition of Breakwater. That’s the key thing. Whilst we were a little premature in getting into the zinc market, in terms of when the cycle actually came around, we would rather be a little early than jumping on a bandwagon too late. No disrespect to companies that are now seeing the opportunity in zinc – they are right to be looking at zinc assets.

P: And I noticed that Nyrstar had reportedly hedged some of their purchases of zinc.

D: Nyrstar is basically a trading company. They own smelters and are very much on the concentrate and metal trading side. They had a desire to be more vertically integrated mining and trading company. That, really, facilitated their push to takeover Breakwater.

D: What we’re seeing now with Trafigura, who are a big shareholder of Nyrstar now and are themselves a smelter and trading company, is more of a move back to their roots. Timing is tough and their acquisition just caught the downside of the market. Trevali, which is kind of the darling of the Canadian zinc producers right now, was somewhat unfortunate with their timing. When they acquired the Santander project in Peru, their first mine, the zinc market was just starting to come off. They’ve done remarkably well through a bearish zinc environment – not just to get that mine up and running, with Glencore’s backing, but also to establish a second mine. That has meant a lot of dilution for Trevali’s loyal shareholders, but they have been able to reap the benefits of that work with the moves this year in their stock price.

P: That’s the challenge of being in production at the right time in the cycle.

D: Absolutely.

P: Sometimes it costs to be a bit early, but I think it is a good price to pay – if you can survive to see the next bull market.

D: If you can be in the right place at the right time, then it’s worth it. An example of that is when Hudbay bought the Balmat mine, which is now on care and maintenance in upstate New York. They acquired that for zero money down – the purchase price was to be paid out of positive cash flow. I think it was a $25M purchase price and they made their acquisition right before that last run in zinc prices. They were able to pay that acquisition price plus a bonus $5M in the space of about 18 months. It’s all about timing.

D: Sometimes things work against you, but anyone that has zinc production right now is well positioned. Any move in zinc prices north of $1 is just gravy on the bottom line. It’s a very good reason that Teck had such strong stock performance this year. Teck has also benefitted from strengthening in the coal and copper markets, but their leverage to zinc prices is higher than on the copper or coal side. Ten months ago, there were concerns about Teck’s debt burden, which pressed it’s market valuation close to $2B dollars, but now their valuation is around $20B. They even came out with a statement recently saying that they expected to have their debt paid down in six quarters!

P: (laughs) Wow!

D: It’s a remarkable turnaround. Especially in these metals that can be especially leveraged to profitability.

P: To follow on that, the industry cost curves that I’ve seen for zinc suggest that current prices are well above the costs. Any further comments on the industry’s production profile?

D: There are not a lot of projects that can be brought back on stream anytime soon. It’s a function of a lack of investment in the sector – it is a very fragmented industry. These mines typically are not big mines. That hit home with Century shutting down – there aren’t many mines the size of Century. You lose a Century, and that’s hard to replace. MMG knew Century was closing and were developing Dugald River also in Australia, with the plan that it would, at least, replace some of Century’s production. There are two big projects due to come on 2019-ish. One is Gamsberg in South Africa, owned by Vedanta (no relation), that I think will produce around 250,000 tonnes. The other is Dugald River in Australia, which is also a couple hundred thousand tonnes.

D: The two biggest mines that can come on stream largely replace the Century production, but that’s it. Those things don’t grow on trees. Arizona Mining are drilling out what appears to be a world-class deposit down in Arizona, but it’s not going to hit this cycle, in terms of development. Robert Friedland’s Ivanhoe Mines in the Congo – has a tier 1, world-class asset in terms of grade and tonnage but, again, it will not come online in time for this cycle. These things cannot be just turned on. The development schedule is substantial. Dugald River was discovered over forty years ago. And it is only going into development now.

D: You will see, to some extent, production that has been shut down coming back online; for example, the 500,000 tonnes at Glencore. There will be a price where they will look at it and think about bringing it back online. They’re smarter than any of us, in terms of the zinc market. If it makes sense to leave some of that production in the ground, then that will be the case. Teck has some fantastic assets where they are more than happy to keep in the ground – they’re not going to be turned on any time soon.

D: I know some very smart people on CEO.CA chat who have analyzed the future supply that can come online and they have the same sense. This won’t be just a two year window. And, once this window is closed, we could see a sustainable zinc price that is considerably higher than the zinc prices we’ve seen between cycles in the past.

P: The supply destruction, so to speak, is a big force in driving that bull market to last for a longer period of time. What about the demand side?

D: Well, all eyes generally turn to China and the USA. US economic growth have helped certain forecasts, in terms of non-Chinese production, but the Chinese situation spooked the metals market earlier in the year. You saw a Chinese growth number that had been widely understood in the mining circles – I think Q4 for 2015 was something like a 5.8% GDP growth rate. That was almost exactly the same as what a Rio Tinto executive had mentioned six months before, but it still spooked the world markets.

D: In January 2016, copper dropped down to $1.95 before slowly recovering and zinc fell to $0.66. I thought that decline in Chinese GDP had been priced into metals when copper fell from $2.60 to $2.20 and zinc had fallen to $0.80! There was a ridiculous knee-jerk reaction to the Chinese number from metals markets, just at a time when the demand side was starting to bite and inventories were dropping. It just goes to show how vulnerable any of these industrial metals are to fears of a slowdown in the economy.

D: That being said, after posting double-digit growth in China for so many years, their economic base is so big that 5.5-6% growth is considerable. The key issue is whether it is on still on the industrial side, or if we start to see consumer-led growth in Chinese GDP. I think that Chinese growth will be sufficient to absorb what production comes from domestic sources, which could be stimulated by higher prices as we discussed before. I think that an improving growth situation in the States and elsewhere should allow zinc, copper, and any of these industrial metals to perform very well in the coming years. And I think we’re seeing that. Since the USA election, the narrative has switched to infrastructure spending and I think we’re going to see the next part of this metals cycle start in the base metals before switching to precious metals. Smart money is definitely starting to move into certain base metal plays.

P: The long-awaited economic recovery, complete with equity markets at all-time highs.

D: I must confess that I am probably amongst a large portion of people who are shocked by some of that market strength, but I like news of infrastructure spending. I will be a huge fan of a “Donald Trump Stainless Steel Fence”. Sorry to all the aggregate companies that wanted to supply all of the raw material.

P: Speaking of demand, I was stunned by how low the zinc consumption numbers are from Africa and wonder if you have any comments on the base metals in the developing world?

D: The early days of the infrastructure spending in China focused on use of lower quality steel. We saw an increase in the use of zinc in Chinese infrastructure as they shifted to better quality stainless steel product – as the cities were built out. I don’t look at Africa as a growth market in the short term. I think Africa has a lot of challenges around the quality of metals that are used. I would rather see advances in agriculture than metal use in Africa, as a continent. People always talk to India and I think, at some point, India will follow China’s lead. There is such vast population density there, but whether we see that in the next five years or further out is hard to say.

D: I know zinc has other uses that are being advanced, such as agricultural markets. Robert Friedland is a big proponent of zinc demand in agriculture – improving zinc nutrients in crops. That is not necessarily a small market. The numbers that have been bandied around for the growth in agricultural uses of zinc over the next few years could amount to 400,000 tonnes per annum. Against a 13-14M tonne market, it is only a few percent, but 400,000 tonnes of new uses of zinc in agriculture are equivalent to another one of these large mines coming offline being required. It’s not necessarily a small impact when you compare it against declines in Western outputs and the limited opportunities to increase zinc production on the horizon.

D: And for all the lithium bulls out there – there are even Australian scientists developing zinc-gel battery tech! Who knows on that front, but I do have a chuckle on that. It would be fun if they could make some advances there. I wouldn’t discount the market for new uses of zinc.

P: Great. There’s a point that is made sometimes around banking and telecomm in Africa, which is: “They won’t replicate the same infrastructure that we have built in the West, they will jump ahead to the next generation of technologies.” You see that in banking with mobile banking and, to some degree, with electricity generation using solar power for particular areas. There are all kinds of challenges in pulling that off, but it’s an interesting concept to suggest that, as these countries start to enter the 21st century, they might skip over some of the things that were standard practice in the 20th century.

D: Well, it’s an interesting point on energy. I remember when I moved out here from the UK and I was involved in a copper deal, back in 1998 when copper fell as low as $0.55. The big thing back then was the electrification of China driving copper consumption. Countries in Africa with ample solar could have a shift in that direction, but it probably bodes better for copper than zinc, to be honest.

P: And a specific question for zinc, any comments on the additives for the high-strength, low-alloy steels?

D: Which additives are you referring to there?

P: Niobium and stuff like that.

D: To be perfectly honest, those speciality metal alloys are not my area. I largely look at the supply-demand picture on the mine side rather than the smelting and concentrate end-products, especially when it comes to the stainless steel market.

P: I would imagine it is hard to work with something that is still being proved out as a game-changer with relatively niche applications.

D: Well, I find it fascinating. I’ve read a lot of the thesis on scandium use, but I’m more inclined to look at things on that can be sold on a bulk scale than as a boutique shop.

P: And zinc has that scale. It boggles my mind that the LME has 18 days’ worth of consumption and that is not considered an extremely low level.

D: For any CEO.CA readers, the zinc panel has what I consider to be the bible of zinc knowledge. It has been prepared by a gentleman named Doug Beattie, who goes by the handle @Ocotilloredux. Doug was Chief Engineer of McArthur River, Cameco’s mine in Canada, but he also worked as an engineer at Glencore’s McArthur River mine in Queensland. It must be something about mines named McArthur River! He’s written ten modules covering zinc mine supply that are just required reading, as far as I am concerned. He also gives a lot of insight on other things.

D: One of the things Doug mentioned on CEO.CA was a study done by a former colleague that suggests a tipping point in zinc inventories is actually around the 25-28 day range. I’m not saying we are at critical levels yet, but we are at levels that support the recent zinc move. The real question is whether we are at a zinc price where we are going to start seeing some of that production, especially the Chinese production, coming online. Will that curtail the run it has had so far? That is the big China question and it’s uncertain. The market seems to be taking most things in stride right now.

P: I saw a graphic that compared weeks of consumption at exchange versus price. There were a few data points from the 2005-2007 time where weeks of consumption was down around 5 and price was up above $2 for zinc.

D: There are a lot of people that are forecasting us to achieve those kinds of price levels again this cycle. The banks tend to show a nice flat, long term average price of zinc, but I’ve also seen 6 or 7 banks that have published bullish reports this year on certain base metals and other commodities. They have highlighted zinc as their most favoured commodity. For example, zinc was one of Goldman Sachs’ most favoured metals and they were forecasting that the price rally would be relatively short-lived. I think they thought Glencore’s production was going to come back on. Goldman had published price projections that that had zinc at $2500/tonne over 3-months, then $2300/tonne for 6-months out, and then $2200/tonne for 12-months. I think those projections anticipated that the higher prices were actually going to induce production to come back online.

D: However, I watch these price projections closely and I noticed last month that Goldman actually switched their projections. Their 3-, 6- and 12-month targets went from $2600, $2700, and $2800/tonne respectively. That’s a $600/tonne swing on their 12-month outlook. I think a lot of people are now starting to wake up to the situation in zinc markets.

D: Although many banks may have a long term average price projection of one dollar pound for zinc, I think we will actually see a much higher sustainable zinc price, when the zinc market does cool down in a few years’ time. I think that is starting to be reflected by more and more of the banks out there. They are starting to recognize these market dynamics, especially on the supply side.

P: I am looking at some of the base case projects that are anticipated to start in 2018 and 2020, like Dugald River and Gamsberg. Those mines are expected to be fairly substantial, around 200,000-300,000 tonnes of zinc annually. There are some even bigger projects on the horizon, but it’s not so clear if they’ll be able to get up to the targeted levels of production. It looks like there is some large production increases expected down the line, but we have had delays in some of those scheduled start dates. Any comment on the tension between the short term and the long term there?

D: Dugald River was originally meant to start in 2016 and I think it might be 2018 now. At one point, Century was planned to come off stream with its 450-500,000 tonnes right when Dugald River was going to come on stream. This was going to help MMG offset 40% of that production loss from Century, but it has been pushed out a little bit. There are lots of things that can happen to delay a project from coming on stream, whether it is permitting issues or whatever else it might be.

D: Notice that the production that was forecast to come off, came off on time. It’s a lot easier to forecast the retirement date of a mine. The two mines you mentioned, Dugald River and Gamsberg, are the two biggest ones that are planned to come on stream and they are only equivalent to the Century mine. Combining the two biggest planned mines replaces only one that has stopped. And that replacement will only start three years after Century went off stream!

D: For some of the other mines, there are still a lot of questions. A couple of the projects are in the hands of smaller companies, so there is always the question of whether they can get finance and be developed. The outlook for projects is what one would expect after a decade of low prices: there hasn’t been a lot of investment in zinc exploration and development. More than likely, we’ll see the same kind of trend that we’ve seen with the likes of Dugald and Gamsberg, in that the development timeline is far more likely to shift backwards than be accelerated forwards. So, that’s why I’m confident that this cycle isn’t going to be the two year cycle that we saw in the late ‘80s and 2005-7. It’s got legs!

D: A lot of smarter people than I suggest that it could be a 3-4 year window. I think that is more likely than two years because one could argue that we’re in the first year right now. Could this market situation extend out to 2019-20? When you look at the projects that could come on stream outside of China, one could argue that, so long as economic growth in the world holds up, supply will get quite critical and support prices for a longer period of time than we’ve seen in the past.

P: I’ve seen some data around the near term delays and reductions in production. Any more comments around the medium term, say 2 to 5 years, and which bigger projects could run out of ore in that timeline?

D: There are certainly other mines that will run out. If I think back to beginning of 2013, I’d look at the world’s top 11/12 zinc mines – we’ve seen 4 of those shut down now in the space of the last couple of years. As I think of the other 7 or 8 on that list, I recall that some were planning expansions but I don’t think any of the other big ones are coming completely off stream in the next 5 years. The perfect storm happened in 2013-15. The key thing is that we’re just not seeing the development in mines to replace even the initial four mines that have come off. That’s the biggest narrative for us.

D: In modern times, this is a pretty unprecedented situation. It’s hard to think of another metal that has faced such a dramatic shortfall in future global production. I’m trying to think of another metal where you could give a “David Letterman Top Ten” list of mines that have come offline in such a short period of time. Copper mines last for eternity it seems. You see lots of projects shuttered because of low metal prices over the years, but they can also be brought back on stream.

D: This perfect storm of so many of those mines coming off stream wasn’t initially recognized the markets. All 4 of those mines came off, then inventories started declining, and it wasn’t until inventories really started accelerating that the market started to become aware of it. We’re really only seeing it now. I think that when zinc broke through a dollar, it was a psychological-level. It’s a headline making level like “Thousand-Dollar Gold!”. Sometimes it takes something like that to wake up the broader market to the opportunity presenting itself.

P: And maybe one last question on it all: The companies that have retired these mines – do you think they are fairly well positioned to survive and to potentially be buyers of the next generation of assets in development now?

D: Whilst it’s a fragmented industry, the three companies that shuttered those big mine operations are doing fairly well. Glencore have got their through their issues earlier in the year and, I think, are well poised to take advantage of improving zinc prices just using the production that they can bring back on. Vedanta shut Lisheen, which was 170,000 tonnes, but they’ve got an expansion in India that they’re considering and have increased the life of one of their other projects by a couple of years; finally they are bringing Gamsberg on stream – they’ll be fine. MMG shut down Century, but they are bringing on Dugald River and that will replace a good portion of that lost production. So, it’s not like MMG are suddenly waking up one morning and finding that they have no exposure to zinc anymore.

D: Zinc is not everyone’s cup of tea and you certainly don’t see the same number of zine producers as you do gold producers or copper producers, but I think those that are in the business understand it well enough to recognize the importance of having a development timeline. Teck, for example, has the Red Dog Mine up in Alaska. They’ve got decades of resources up there. Whilst they are still developing their existing operations, they’re secured assets for decades into the future. They bought out Rox Resources interest in Teena and that is a fantastic project in Australia that will stay in the ground for many years to come. Again, I think the players in the zinc market understand the importance of the metal to their bottom line and their role as key players in the industry. It’s not quite an oligopoly, but when you look at Glencorp, MMG, Teck, and Vedanta versus non-Chinese production, they’re the key players.

P: I understand that zinc is produced as a by-product, and I wonder if some of the people who are involved in the zinc market are there as an after-thought in some way?

D: You make an interesting point from a by-product standpoint. I think we’d see a lot more little bits of zinc here and there hitting the market if silver prices were higher. A lot of silver projects in Mexico have lead-zinc components. The lead, sometimes zinc, that’s associated with the projects are important by-products but we’re not seeing a lot of that production or potential production coming on as silver prices have also been depressed for several years now. There will be some by-product production that will come back on stream as silver prices improve in years to come. For now, I find it interesting to note that companies are suddenly – left, right and centre – including the zinc assays alongside their copper and precious metals assays in the headlines of their news released: “Oh everyone we’ve got zinc too!” Always a good sign that you’re in a zinc market.

P: Doug, thank you very much for talking with me about the zinc markets today.

D: My pleasure, Peter.